Payments Industry Outlook: The Role of Risk Management in Promoting Expansion

The payments industry is at the cusp of a transformative era, driven by rapid technological advancements, changing consumer preferences, and evolving regulatory landscapes.

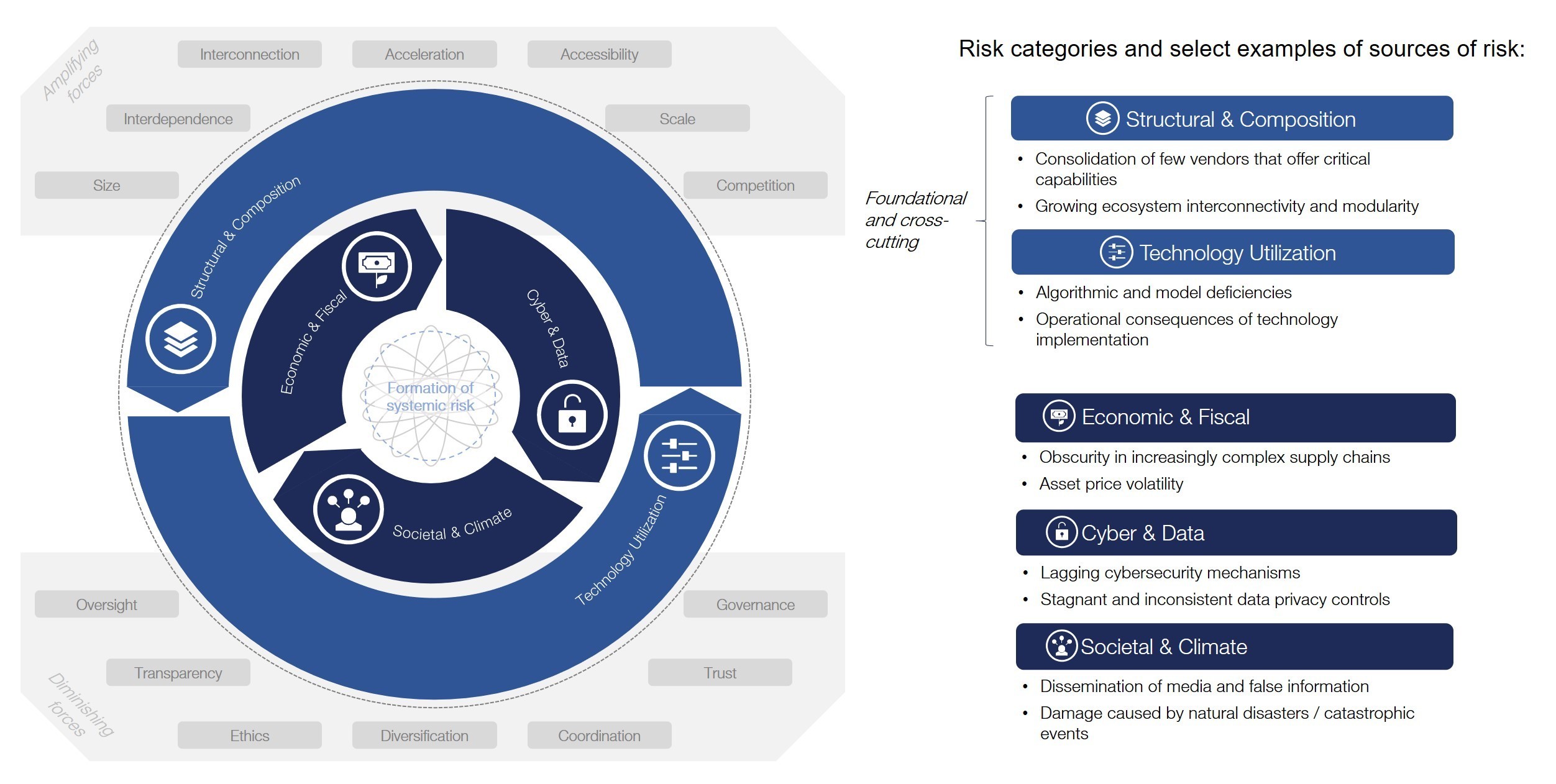

As we move deeper into the digital age, managing risk not only becomes necessary for security but also a potent catalyst for growth.

In an era where data breaches, fraud, and cyber threats loom large, the ability to effectively manage risk can be the key differentiator between success and failure in the payments sector.

This duality of risk management, protecting against threats while enabling expansion, forms the backbone of the future payments landscape.

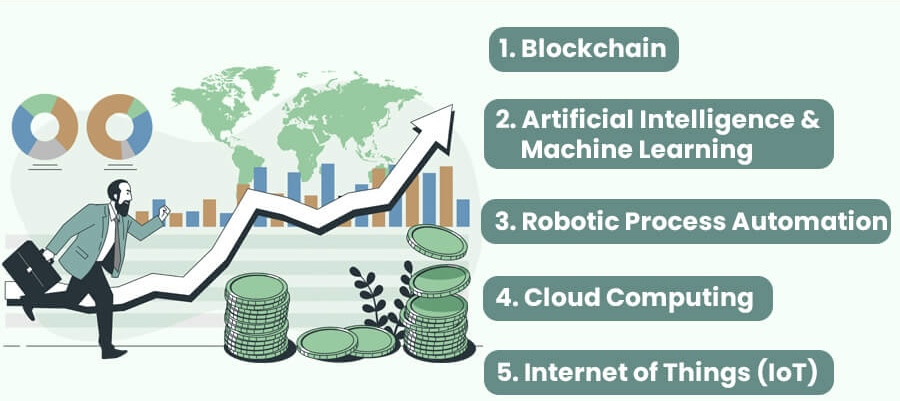

i. Growth Through Innovation

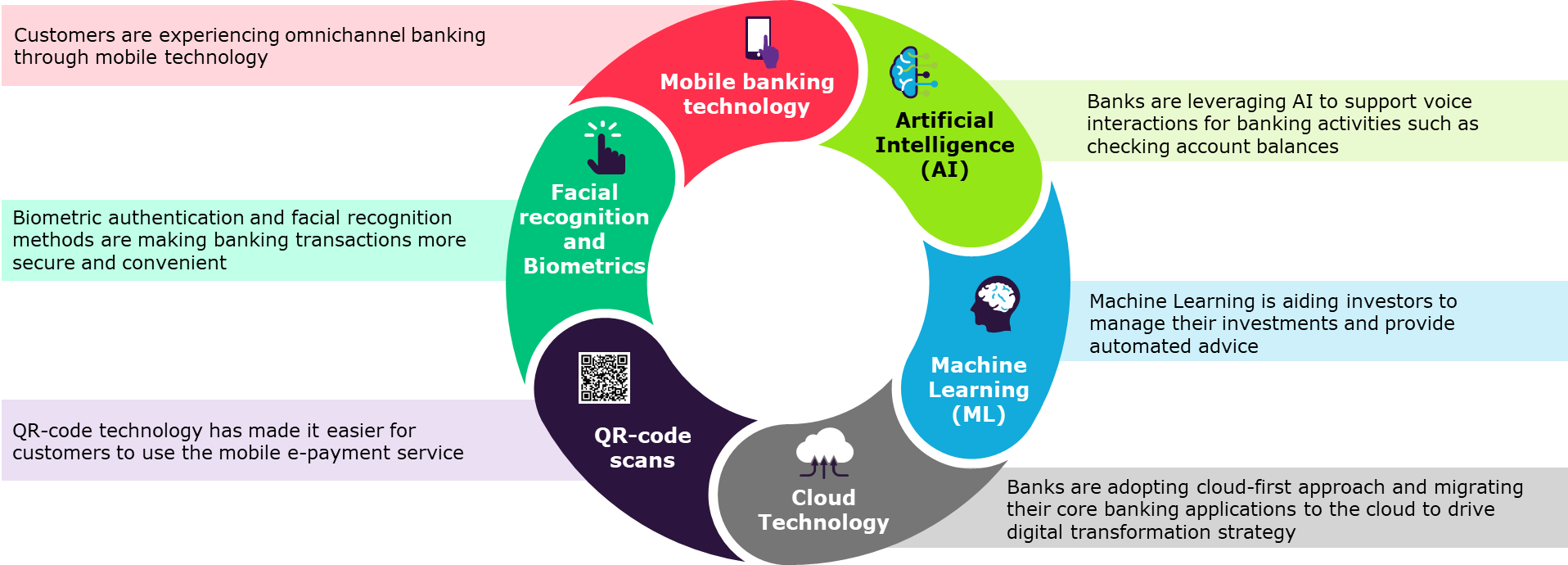

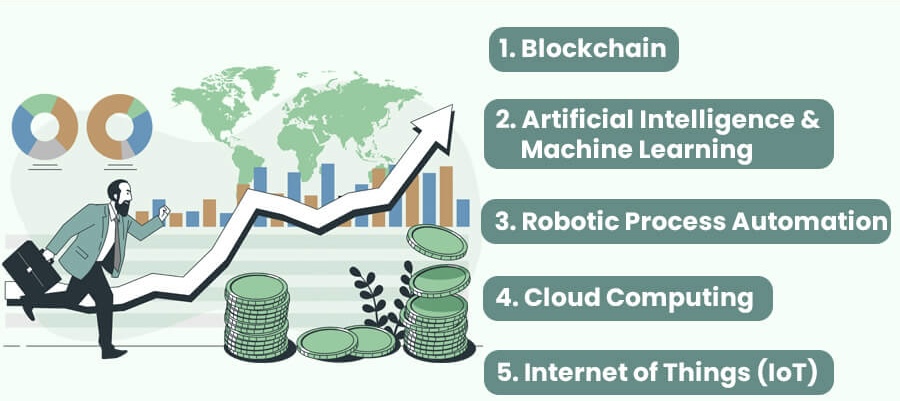

The payments industry has embraced technologies such as mobile payments, blockchain, artificial intelligence (AI), and contactless transactions. These technologies streamline processes, enhance user experience, and expand the scope of what financial transactions can look like. However, with innovation comes new vulnerabilities—cyber risks, regulatory challenges, and strategic risks from rapidly changing market conditions.

ii. Emerging Trends in the Payment Industry

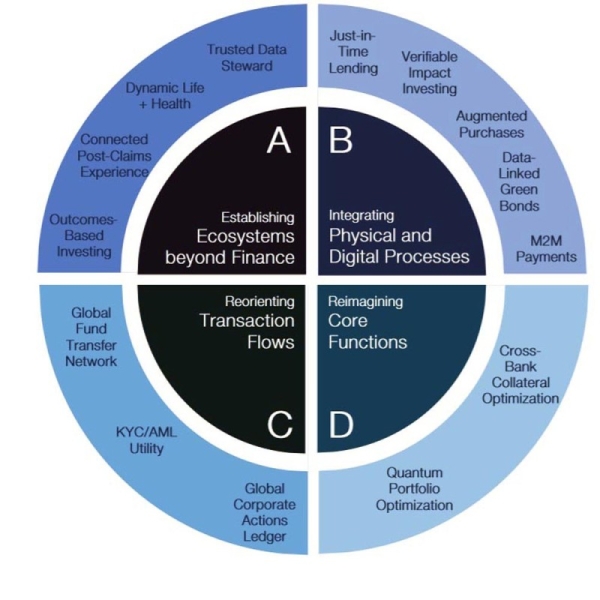

The global payment landscape is shifting dramatically, marked by key trends such as the rise in digital payments, the adoption of blockchain technology, and the increase in cross-border transactions. These advancements offer immense opportunities for growth but also present novel risks that need to be managed.

A. Digital Payments Expansion

The surge in e-commerce and mobile banking has accelerated the adoption of digital payments. While this promises convenience and broader market access, it also heightens risks related to cybersecurity and data privacy.

B. Adoption of New Technologies

Technologies like blockchain and cryptocurrency are transforming traditional payment models. They offer advantages in terms of transparency and reduced transaction costs but also pose regulatory and operational risk challenges.

C. Regulatory Dynamics

As digital payments grow, regulatory scrutiny intensifies. Compliance with these regulations is crucial for maintaining consumer trust and operational continuity.

iii. Key ways that managing risk can drive growth in the payments industry

o Enhanced security builds trust: Consumers are increasingly concerned about the security of their financial information. By implementing robust risk management strategies, businesses can build trust with their customers and encourage them to transact more frequently.

o Fraud prevention reduces costs: Fraudulent transactions can lead to significant financial losses for businesses. By investing in fraud prevention measures, businesses can protect their bottom line and free up resources for growth initiatives.

o Data-driven decision-making leads to better products: By leveraging data analytics to identify and assess risks,businesses can develop new products and services that are tailored to the specific needs of their customers.

o Compliance with regulations ensures smooth operations: The payments industry is subject to a complex web of regulations. By ensuring compliance with these regulations, businesses can avoid costly fines and disruptions to their operations.

iv. Leveraging Risk Management as a Strategic Tool

A. Risk Identification and Mitigation Drives Trust

Trust is foundational in the payments industry. Consumers and business partners need assurance that their financial transactions are secure. Effective risk management helps companies build this trust, turning it into a powerful competitive advantage. By demonstrating commitment to safeguarding data and ensuring transactional integrity, companies can differentiate themselves.

B. Regulatory Compliance Stimulates Innovation

Staying ahead of regulatory changes is a huge challenge. However, those who manage to not only comply with but also anticipate regulatory shifts can use it as a launching pad for innovation. Regulatory knowledge can provide insights into future industry trends, helping businesses to be the first movers in developing compliant, cutting-edge solutions.

C. Utilizing Big Data and AI for Predictive Risk Management

With the vast amounts of data generated by digital transactions, payment companies have a goldmine of insights at their fingertips. Using AI and machine learning, these companies can predict and preempt potential breaches. This proactive approach not only mitigates risks but also boosts operational efficiency, reducing costs and improving processing speeds.

v. Strategic Partnerships Expand Capabilities and Safety

Collaborations between payments firms and cybersecurity specialists, fintech startups, and cross-industry tech giants can mutually enhance technological capabilities and security frameworks. These partnerships allow sharing of best practices, risk intelligence, and cutting-edge security technology, thereby distributing the burden of risk and enabling more substantial innovation.

vi. Education and Consumer Awareness Fuel Sustainable Growth

As technology evolves, so does the sophistication of cyber threats. Educating consumers about the risks associated with digital payments and how to guard against them becomes crucial. Increased consumer awareness results in safer transaction behaviors, reducing fraud and building a more secure payments ecosystem.

vii. The Role of Resiliency in Future Growth

The ability to quickly recover from security breaches and adapt to new threats is as important as preventative measures. Resilient systems and processes enable payments companies to maintain continuity, minimize downtime, and protect consumer data efficiently, all of which are critical for long-term growth.

viii. Conclusion

The future of the payments industry shines brightly, lined with innovative technologies and potential for expansive growth. However, the path is laden with risks that must be skillfully managed.

By turning risk management into a strategic initiative, companies in the payments sector can not only defend against potential threats but also leverage these challenges as growth opportunities.

This proactive and strategic approach to risk will not only ensure safety and compliance but also drive innovation, market expansion, and ultimately, robust business growth in the evolving digital payments landscape.

In the journey towards the future of payments, effective risk management will undoubtedly be the cornerstone of success.

ix. Further references

The future of the payments industry: How managing risk can drive growth

LSEGhttps://www.lseg.com › insights › to…Top five payments industry trends to watch in 2024

McKinsey & Companyhttps://www.mckinsey.com › how-…Risk & Resilience consulting

Deloittehttps://www2.deloitte.com › …PDFThe future of risk in financial services

FutureCIOhttps://futurecio.tech › how-paymen…How payments and risk management are evolving

PwChttps://www.pwc.com › publicationsPayments 2025 and Beyond

FIS Globalhttps://www.fisglobal.com › future…The Future of Payments in Five Charts

GOV.UKhttps://assets.publishing.service.gov.uk › …PDFFuture of Payments Review

KPMGhttps://kpmg.com › articles › risin…Rising Financial Crime Risks in Digital Payments

PwChttps://www.pwc.com › publicationsEmerging Markets: Driving the payments transformation

i-spiral.comhttps://www.i-spiral.com › mitigatin…Mitigating the Risks in the Payments Industry –

KPMGhttps://assets.kpmg.com › pdfPDF10 predictions for the future of payments – KPMG LLP